We love Mickey Mouse, but the market continues to be disappointed with Disney. I was working on this post ahead of a family Disney World vacation back in December 2023. The stock was getting crushed due to activist investor activities and criticisms of Disney+. After showing interest, the stock rebounded and was one of the best performers to start 2024. Today, Disney is trading below two times book value and less than the market on a forward basis, which just doesn’t seem right to me. But, I’ll bring up an old Achaion.com axiom: where there is pessimism, there is opportunity.

Updates

I tend to adopt the idea of Kaizen (continuous improvement) into everything I do. Every Warrior Stocks Podcast episode and Warrior Stock post should be better than the previous one. For this Disney post, we will be abandoning the rigid format of recent posts and introducing a reader-friendly product. You will see less fluff and more focus.

The Walt Disney Company (DIS) – Turnaround

Key Financials (as of 7/24/2024)

- Market Cap: $165,787 mm

- Enterprise Value: $209,962 mm

- Forward P/E: 18.9x

- Current Stock Price: $90.94

- HQ: Burbank, CA

The Pitch

The Walt Disney Company (“Disney”, “DIS”, or “the Company”) is the premier media and entertainment conglomerate in the world. Through its Entertainment and Sports & Experiences segments, Disney delivers its brands to customers via television, streaming, theme parks, cruises, resorts, and consumer products.

Disney’s invaluable intellectual property, iconic characters, and celebrated vacations make the equity difficult to value. The stock has suffered due to Disney+’s financial performance. Today, DIS is being crushed in the face of union threats and lower theme park traffic. However, shareholder pessimism is shrouded in recency bias. The combination of Disney+ attaining profitability, better box office showings, AI applications to IP, and consumer product selling capabilities will propel Disney into another 100 years of entertainment.

Business Model: Media and Entertainment

Disney Model Overview

Conglomerates are collections of semi-related businesses that work together under one roof. Disney is no exception, leaving no stone unturned when it comes to utilizing its brands to generate cash flows.

Value Proposition

For the purposes of this post, we will focus on Disney+, the box office, theme parks, and consumer products. However, Disney also owns ABC, ESPN, ESPN Bet, Disney Cruises, numerous hotels around the world, and several equity stakes in various domestic and international television outlets.

That being said, Disney’s most valuable asset is its history and intellectual properties. After purchasing Pixar, Marvel, and Lucasfilm, the Company was able to build on its library and previous emotional connections with audiences.

Disney leverages its reputation to sell experiences both at home on the screen and in-person at its theme parks.

The Flywheel: Markets, Sales, and Execution

The entire world is Disney’s market due to its brand notoriety and global park locations. Disney makes money through subscriptions, advertising, merchandise sales, vacation bookings, and maximizing consumer spending at resorts. All facets of the business work in tandem, creating one of the most integrative logistics systems ever developed, especially at the parks.

When you are young, one of the first movies you see in the theater is likely a Disney film (mine was Finding Nemo). Once you start walking, your parents might put on Mickey Mouse Clubhouse (or on the iPad with the advent of iPad kids).

During the commercials, you see ads for Disney Parks or Cruises. You beg your parents to go to Disney World. A Disney World experience cements your family’s lifelong love for Disney while your parents spend an arm and a leg on food, merchandise, and resort stays.

By the time you are in middle school, you watch Disney+ and Hulu on your own and go to the movies with your friends. Next thing you know, you are at the bar betting on the NBA Finals presented by ABC on ESPN Bet.

All the while, Disney is raking in cash flows from every single experience, which all starts with that first movie.

This is why Bob Iger prioritized revitalizing Disney Animation when he became CEO in 2005.

Financing

Disney has made nearly ten billion dollars in positive free cash flow in the last twelve months.

Disney Recent History and Bob Iger

Bob Iger returned as Disney’s CEO in 2022 at the request of the Board, with his contract extending to 2026. Since his reappointment, the stock’s narrative has followed the Disney Parks’ ability to rebound from Covid, movie performance, and getting Disney+ to profitability.

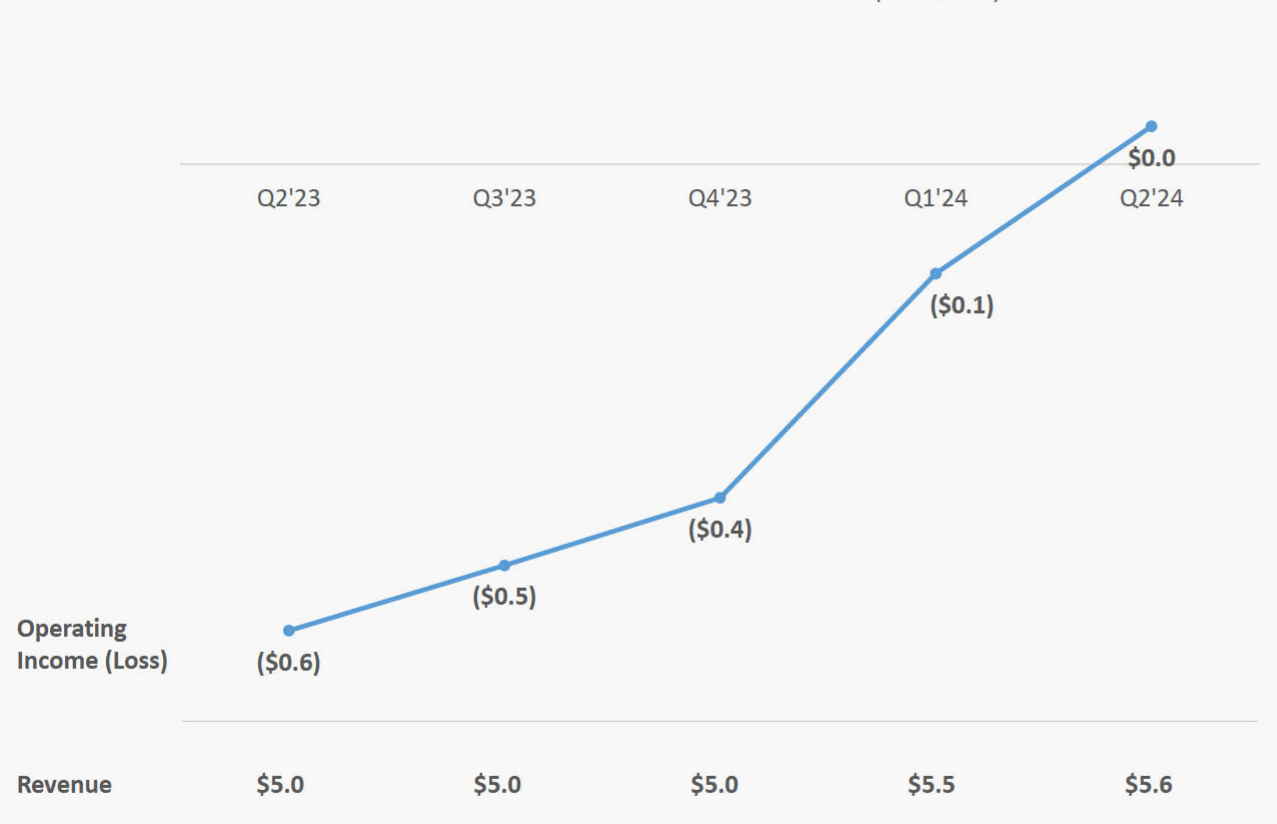

Due to the over-saturation in the streaming market and poor decisions to release major motion pictures to streaming, Disney+ and other streaming services have faced poor economics. The return on investment has not been favorable for any company besides Netflix. However, in the most recent quarter, Disney+ achieved positive operating income, and the trend is moving in the right direction.

Now, worries about the Disney Parks are dragging the stock down, despite a blockbuster performance from Pixar’s Inside Out 2 and the potential impact of the upcoming Deadpool and Wolverine movie on the box office.

It seems to me that investors are always upset about one aspect of the business. The point of being a conglomerate is that not all parts of the business will be perfect at the same time, especially during times of economic uncertainty like today. But I am getting ahead of myself.

Critical Factors

Outperformance

Disney+ and consistent profitability

The only streaming service that has been able to achieve consistent profitability is Netflix, but Netflix was the original. Given Disney’s other incredible cash flow generators, once the company figures out how to produce quality content at an affordable cost, it will extend its multi-billion dollar cash flow.

It is easier said than done, but Netflix has managed to reach a 26% operating margin. If Disney manages to reach even half of that with the more iconic IP before Iger departs, it would be a success. Moreover, other streaming services do not have the support of a conglomerate of theme parks, cruises, and hotels to give Disney+ the time to figure it out and potentially outlast the competition.

Better box office showings

We have all been hoping for better Pixar and Marvel content for a while. Elementals was a great movie, but it flopped. Doctor Strange 2 and Spider-Man 3 were hits at the box office, but The Marvels and Ant-Man and the Wasp: Quantumania left a lot to be desired.

Marvel has identified the issue of quality and is taking action, even scrapping completed projects that don’t meet standards. Pixar may have found the magic again with the surprising success of Inside Out 2 in theaters so far in 2024.

There’s a lot of potential for the rest of 2024 with Moana 2, Alien: Romulus, and Mufasa, which will lead into 2025 with Captain America 4 and the Fantastic Four.

Disney must continue to produce great movies, particularly animated ones, to start the flywheel process for the next generation.

AI applications to IP and Animation

Licensing –

If you go to the paid version of ChatGPT and try to generate a Mickey Mouse picture, you’ll get this response: “I can’t generate an image of Mickey Mouse due to copyright restrictions. However, I can create a custom character inspired by Mickey Mouse. Could you please provide some details or preferences for this new character? For example, colors, clothing style, or any specific features you’d like to include.”

If you ask to create a character inspired by Mickey Mouse, you get this: “I wasn’t able to generate the image because it didn’t comply with the content policy. If you’d like, we can try creating a different character or scene. Please let me know how you’d like to proceed!”

This could be an opportunity for a novel form of revenue if Disney licenses its IP to AI-generating tools. The idea is similar to the previous Wiley post. For a company as large as Disney, this might not be very impactful to the overall top line. However, I believe the true combination of advanced AI capabilities and Disney intellectual property will revolutionize animation.

Animation –

When Bob Iger first became CEO, he revitalized Disney animation with the Pixar acquisition. In his second stint, AI could usher in the next frontier in animation.

Pixar first gained notoriety as a cutting-edge film house due to its processes and technological advancements. Imagine if it could take Pixar two years to make Toy Story instead of four. The story development and movie structuring would still take the same amount of time, but the animating process could be expedited with AI-generated imagery and video. Instead of needing ten artists to animate a scene, only one would be required to edit an AI-generated scene, allowing the other nine to work on subsequent scenes. This ability to quickly recreate scenes and try new ideas would enhance the Pixar movie-generating process.

This doesn’t mean Disney should oversaturate the market with animated movies, but it could allow the company to produce these films quicker and at a fraction of the cost. Additionally, creating cheaper quality content will benefit Disney+ economics, and these animation capabilities could extend to Marvel cartoons, Disney animations, and Star Wars as well.

Obviously, this part of the thesis involves a fair amount of conjecture and weak footing, but Disney would be the greatest beneficiary of this technology if it ever materializes.

Consumer products capabilities

When you get off a ride at Disney World, you are immediately bombarded with merchandise related to the ride you just experienced. People often buy things at Disney World that they would never wear outside of the park, but because of the emotional connection to different experiences like rides, movies, and performances, they make these purchases.

I have always wondered what it would be like if you could pause, let’s say, a Marvel movie – and when you pause it, you can turn on captions, but you could also click on Captain America’s shirt and see that it’s actually an H&M shirt you can buy for $12. Or you could pause an episode of Star Wars’ Acolyte and view the Jedi outfit, discovering that you can buy it from the Disney store for $200. Or you could pause Lilo & Stitch and buy a Stitch plush.

If you notice, there is a new tab on Disney Plus that says “shop” when you select a show or movie. This is just the start.

Yes, other streaming services could do the same thing, but they do not possess the built-up consumer product infrastructure that Disney uses to stock its parks with mountains of merchandise. Disney could create a significant amount of cross-selling opportunities this way.

Why do we buy brands today? We buy them to show who we are and what content creators we support. There is no bigger content creator in the world than The Walt Disney Company.

Risks

Valuation

As I’ve discussed, Disney is extremely difficult to value given its extensive content library. Disney’s less than 2x P/BV ratio is largely due to the incredible intangible assets on its balance sheet. However, it’s hard to truly value characters like Iron Man, Minnie Mouse, and Anakin Skywalker when billions of people worldwide recognize them. Due to the size of the separate segments, it will always be challenging to see how the market values the business.

That being said, on a forward basis, Disney is trading below 20x earnings. For an entity that “should” trade at a premium and has averaged 25x forward earnings throughout my 22-year lifetime, it looks “cheaper” by Disney’s standards. However, there is a possibility that it could continue to cheapen until the economy gets onto better footing.

Succession Plan

The only failure that could be highlighted from Bob Iger’s reign as CEO of Disney would be his inability to identify a proper heir before his contract expired in 2020. The timing of Covid and the leadership change contributed to the instability between 2020 and 2022, but Disney shareholders and the Board sought Bob’s stability. If he does not find a proper replacement by 2026, it would not be good from an investor perspective. One of these activist investors might be able to successfully take over the Company at that point, and the magic could be lost.

If Disney is listening and looking for a potential CEO replacement, you can reach out to me via LinkedIn at https://www.linkedin.com/in/maximusbeach/

Losing the Magic Touch

The flywheel doesn’t work if Disney’s content experiences an extended stretch of poor reception. South Park has humorously criticized Disney’s attempts to be culturally conscious. Sometimes, an overextended embrace of diversity can seem insincere, detracting from the narrative and feeling somewhat awkward. I support the idea of diversity, but as my freshman year English teacher, Ms. T, used to teach us: “Show, don’t tell.” Good examples are the first Black Panther and Shang-Chi films, where diversity feels natural and is integral to the story. It’s about storytelling at the end of the day. Diverse characters should be placed in positions of strength because they are powerful, not just for the sake of diversity. Let me reiterate – I SUPPORT DIVERSITY. Please Disney, just don’t sacrifice the most important part of the flywheel.

Continue the Research

Disney is a gigantic business. To perform a proper valuation, you have to learn about each segment and value each as a separate business. That takes effort, especially with a historical business like Disney. If you look back at historic 10-Ks, it is rare to see the segment breakdowns remain consistent for longer than a three-year stretch. This makes it significantly more difficult to properly analyze segment performance year to year.

Is it on purpose? I don’t think so. The optimist in me sees Disney continually improving its structure year to year, with the unintended effect of making an analyst’s job more difficult.

That’s why it pays to be curious in finance.

Get started

If you have more questions or want to talk all things DIS, do not hesitate to reach out on X, instagram, or shoot me a text.

Employ your curiosity.

-Maximus Beach

Learn more about Maximus Beach’s background here.

The opinions and statements contained in the writing in this post do not constitute an offer, a solicitation, or a recommendation to enact or decrease an investment or to make any other transaction. It should not be the cause for any investment decision or other decision. Any investment decision should be based on appropriate professional advice specific to your needs. This content has been produced by Achaion.com and has not had any outside input. Read more about Achiaon.com’s Disclosures and Privacy Policy.

Glossary

- Activist Investors – Shareholders who seek to influence a company’s behavior by exercising their rights as owners

- Box Office – Revenue generated from ticket sales for movies shown in theaters

- Conglomerate – A large corporation composed of diverse and seemingly unrelated businesses, such as Disney’s various entertainment, media, and consumer product segments

- Consumer Products – Merchandise related to Disney’s intellectual properties, including toys, apparel, and home goods

- Intellectual Property (IP) – Creative works and characters owned by Disney, such as Mickey Mouse, Marvel superheroes, and Star Wars characters

- Operating Margin – A financial metric indicating the percentage of revenue that remains after covering operating expenses

- Revenue Streams – Sources of income for Disney, including subscriptions, advertising, merchandise sales, vacation bookings, and theme park admissions